The April jobs report was widely viewed as pushing the Fed's "liftoff" at least several months into the future. Although it came in close to expectations (223K vs. 228K), downward revisions to February and March dampened enthusiasm. But that's old news—we knew the economy was weak in the first quarter. What counts is that jobs growth has bounced back and the economy is not sinking: the slump is behind us, as I noted earlier this week. So on balance I think this was a decent report.

Jobs growth bounced back in April, following a slump in March, much as I anticipated. We'll probably see a stronger report next month. These things happen; what's important is that the economy's fundamentals haven't changed. It's still the slowest recovery on record, but the economy does continue to expand.

The current pace of jobs growth is within a range of 2 - 2.5%, which is very much in line with what we have seen the past several years. There's a hint of improvement in the past six months, during which the annualized pace was 2.6%. If this continues, the Fed will be in liftoff mode within months.

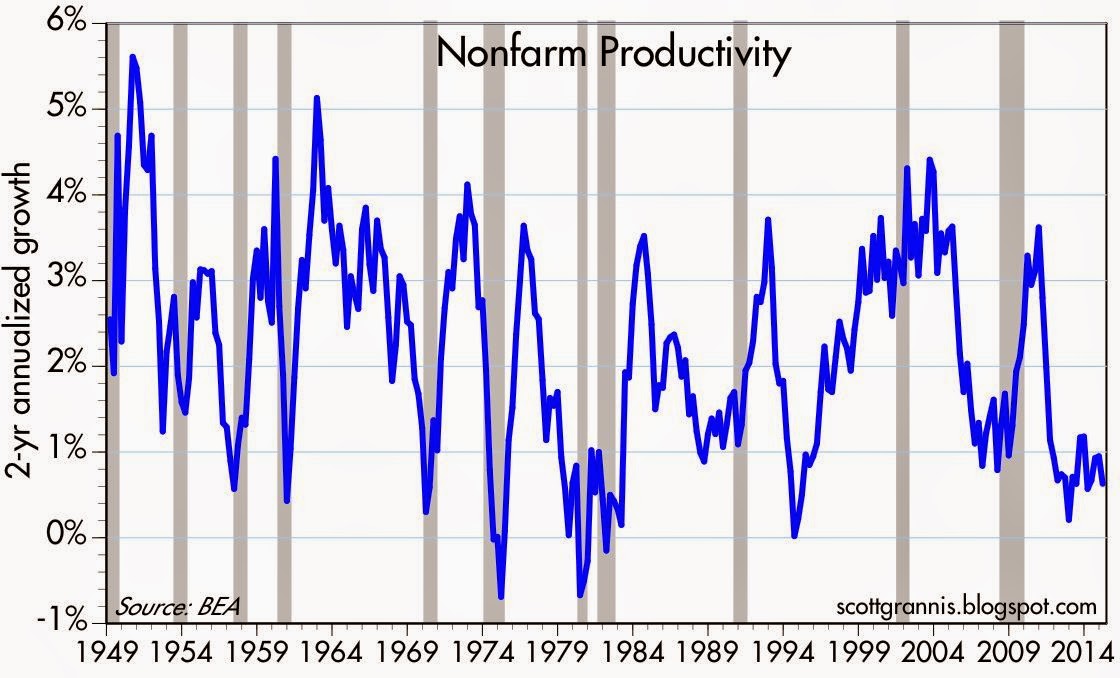

One very encouraging thing is the lack of growth of public sector jobs—no growth at all for the past nine years, in fact, opposite a gain of almost 6 million private sector jobs over the same period (see the first of the above two charts). This has contributed to the decline in federal spending as a % of GDP (now only 20.5% vs. 24.5% six years ago), and it is giving more space for the private sector to grow, which in turn augurs well for future productivity gains. That would be a very good thing, since, as the second chart above shows, productivity has been miserably weak for several years running. What the economy really needs is a confidence boost, and increased business investment. Cutting the corporate tax rate seems like a no-brainer that only Washington can fail to appreciate.

Even though this is the weakest recovery on record, it's now set a new record for job security: the lowest ratio of weekly unemployment claims to the workforce. A typical worker is less likely to lose his or her job today than at any time in the past 50 years. Downside risks have declined measurably, but we're left wondering how long it will take policymakers to discover the key to unlocking the economy's tremendous upside potential.

No comments:

Post a Comment