As the chart above shows, the price of oil has jumped by one-third in the past three weeks. This takes a lot of pressure off the oil patch.

Higher oil prices have helped spreads on HY energy debt to narrow by almost 500 bps! This is a clear sign that panic is receding.

A major contributing factor to the bounce in oil prices is the huge drop in the number of active drilling rigs in the U.S., which has plunged by 75% in the past 14 months. The cure for low oil prices is low oil prices, which have sent the message to producers to shut down production and exploration.

This same dynamic (supply and demand coming into balance) is playing out in the metals markets. The CRB Metals index (see above chart) is up 10% in the past two months. This suggests that the Chinese and global economies are not going down a black hole. Producers are cutting back and consumers are ramping up demand in response to lower prices. Markets work!

The service sector is also not going down a black hole. Although the readings from the ISM surveys show the service sector is relatively weak, it is still growing. The Business Activity index, shown above, bounced quite a bit from its January low, which suggests that sentiment (e.g., everyone's worried these days, but the worry index is going down of late) could be playing a role in the relatively weak readings. It's also the case that most of the weakness can be traced to the energy sector, which contributed an additional 25K layoffs last month, according to the Challenger survey of announced corporate layoffs.

Weekly claims for unemployment have probably fallen as much as they are going to. The recent uptick is minor, and likely reflects a final round of energy-sector layoffs.

The ADP estimate of February private sector payrolls (blue line in the chart above) suggests that jobs growth continues at the rate which has prevailed for the past several years. No deterioration, no improvement. Steady as she goes may be boring, but it is good news when the market is worried about a recession.

With the news coming in better than feared, the market has managed to rally.

But as the chart above suggests, there is still a lot of concern out there. Gold and TIPS prices have jumped as the world worries that central banks will try once more to goose their economies with more QE and negative interest rates.

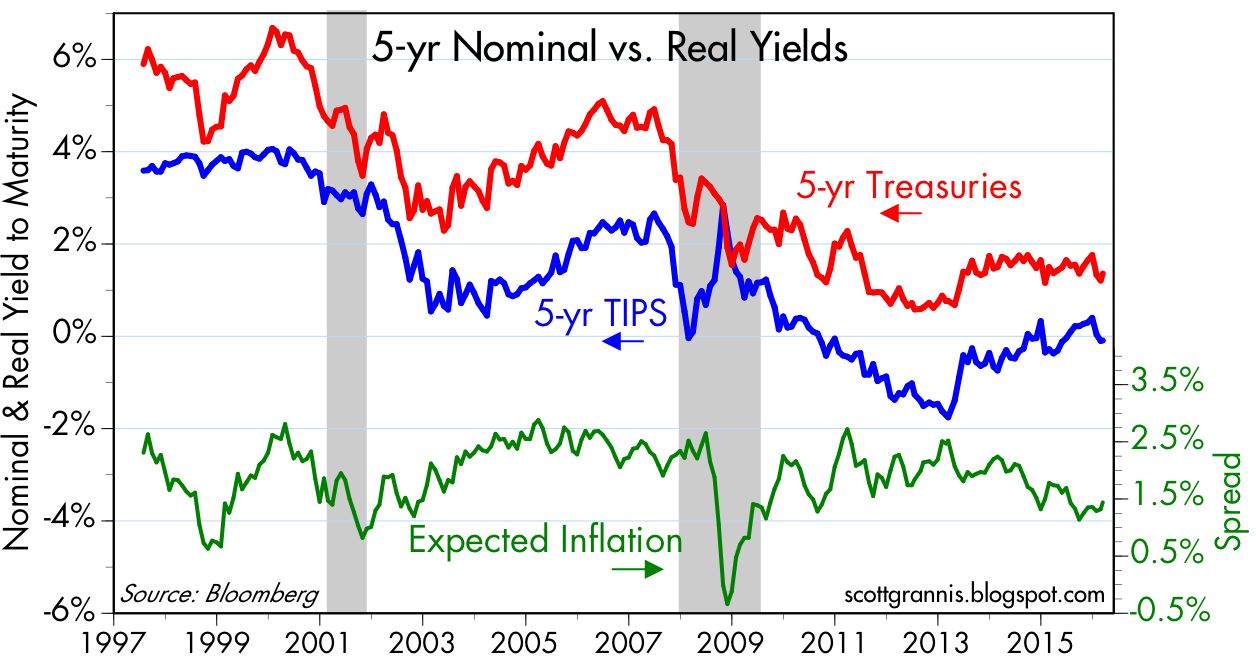

With the bounce in oil prices, we've also seen a bounce in inflation expectations. Breakeven spreads on 5-yr TIPS have jumped almost 45 bps in the past three weeks. Now at 1.44%, they are a bit below their long-term average of 1.9%, but not seriously below. In essence, the threat of deflation has almost gone up in smoke, according to the bond market.

No comments:

Post a Comment