Time for a review of some key charts that I'm following. On balance, I see evidence that inflation is running about 1 ½% to 2%, as it has for the past 15 years or so. I find very little, if any, evidence that monetary policy is too tight or that deflation is likely or a real threat. This suggests that the market is overly concerned about the Fed "running out of ammunition," and overly concerned about the risk of a "downward spiral" that might be sparked by an outbreak of deflation (i.e., people stop spending because money acquires more value with time). It all but rules out the need for negative interest rates, which could be potentially dangerous since their purpose is to destroy the demand for money, and it suggests that the Fed was justified in making a modest increase in short-term interest rates. I also see reasons to think the market may be too pessimistic about the outlook for economic growth.

The Consumer Price Index and the Personal Consumption Expenditures Deflator (above charts) tend to track each other, with the CPI running about 30-50 bps higher the the PCE deflator due to differences in the basket of goods and services measured by each. In the past year or so, both measures dipped close to zero, due mainly to collapsing oil prices, but they have recovered significantly in recent months. Meanwhile, the core and ex-energy versions of both have been relatively stable: the CPI ex-energy is up 2% in the year ending January '16, and the core PCE deflator is up 1.7% over the same period. Both have accelerated a bit of late, which runs counter to the prevailing notion that inflation is dead. With oil prices stabilizing, it's therefore

quite likely that the headline CPI will hit 2% within a few months, and the PCE deflator will be close behind. In the world of macroeconomics, this is as close to the Fed's target of 2% on the PCE deflator as one could hope for, and there is no reason for a shortfall of even ½ % to be of concern. Arguably, the ideal rate of inflation would be 0-1%, but I'd be happy with 1 ½%.

As the chart above suggests, one important source of low inflation over the past 15 years has been declining prices for durable goods (e.g., computers, electronic gadgets, appliances). Durable goods prices on average have fallen by one-third since 1995. At the same time, the prices of "services" (which are mostly driven by the cost of labor) have increase by more than two-thirds. Thus,

the deflation of durable goods prices means that an hour's worth of labor buys two and a half times more durable goods today than it did in 1995. The source of this "deflation" can be traced rather easily to China, which became a significant exporter of cheap durable goods beginning in 1995. (Durable goods prices never experienced a sustained period of decline prior to 1995, by the way.) The collapse of energy prices in the past year or two shows up in flat to declining prices of non-durable goods, which have depressed inflation of late.

It's a mystery to me why folks like Donald Trump say that China has been stealing our jobs, when thanks to cheap Chinese goods the purchasing power of the entire country has increased significantly.

So: is inflation low because the Fed been too tight? I think not. Inflation has been low mainly because of supply shocks: China's export boom, and fracking technology which has significantly boosted oil production, which in turn has resulted in collapsing oil prices.

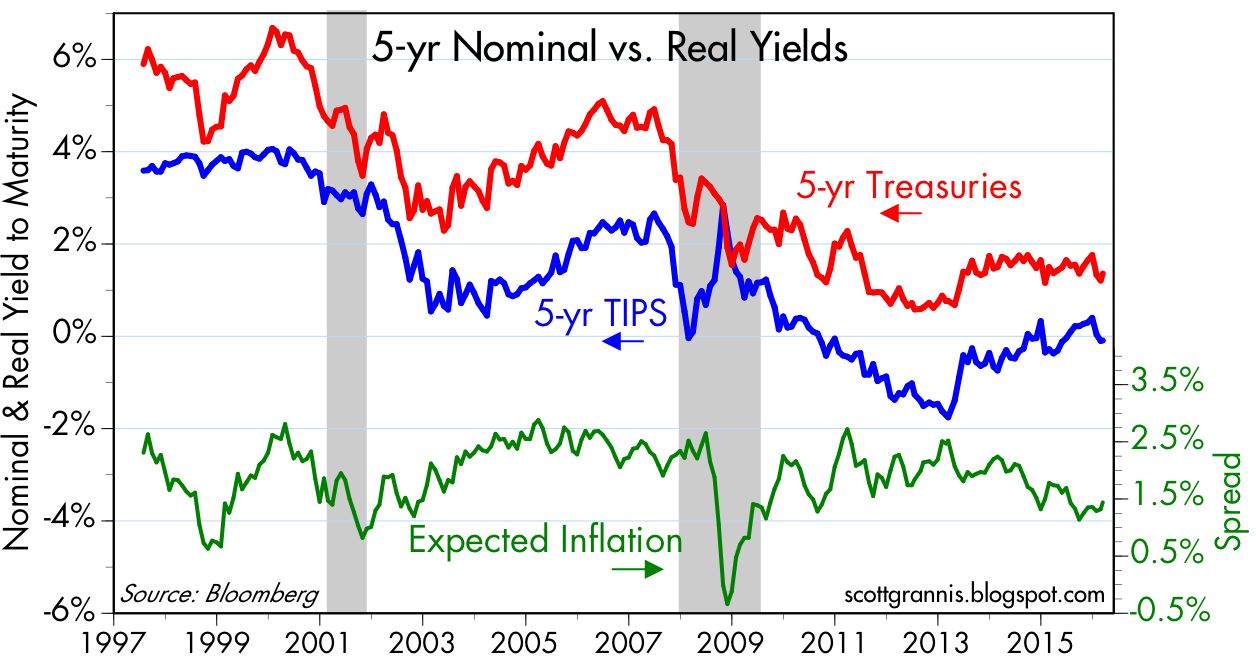

The chart above shows the market's expectation for the average annual inflation rate over the next five years (green line), as derived from the yields on 5-yr Treasuries and 5-yr TIPS. Currently 1.32%, expected inflation is lower than the current level of core inflation, and lower than the 2% average inflation rate of the past 15 years. If anything, this suggests the market may be underestimating inflation. If so, then it would stand to reason that the bond market is quite vulnerable to any sign of rising inflation.

With 10-yr Treasury yields currently a mere 1.73%—only 25 bps above their all-time lows of mid-2012—the bond market is priced to slow-growth, low-inflation perfection;

it's vulnerable to any sign that inflation is either not falling or rising, and/or any sign that economic growth is, say, 2% or better. Extremely low Treasury yields are also a good sign that the market is consumed by pessimism, given that the earnings yield on equities is 5.7%. Choosing 10-yr Treasuries with a yield of only 1.7% in lieu of equities yielding 400 bps more (and considering further that equities have far more upside potential than bonds at this point) only makes sense if one is convinced that earnings will suffer significantly in the years to come. So far, earnings are down only a little more than 2% in the past 12 months, and most of that is coming from the oil patch. Put another way, the current PE ratio of the S&P 500 is 17.4, whereas the PE ratio of the 10-yr Treasury is 58! To pay so much for the presumed safety of Treasuries is to have truly dismal expectations for economic growth and corporate profits.

About 10 years ago I put together the chart above in order to illustrate how tight money (as reflected in rising real short-term interest rates) and high and rising oil prices conspired to trigger the recessions of 1990-91 and 2001. (As I described it then, the economy gets "squeezed" by expensive money and expensive energy, as illustrated by the blue and red lines converging.) The same thing happened with the recession of 2008-9, as oil prices reached record-high levels and the Fed raised the real Fed funds rate (its primary policy tool) to over 3%. If tight money and expensive oil have traditionally been bad for the economy, then today's negative real rates and cheap oil prices are likely a godsend. This suggests that the economy can do better than the market expects, even if it only continues to grow at 2 -2 ½%, as it has since 2009.

The chart above illustrates how Fed tightening has preceded every recession since the late 1950s. Recessions have always followed the confluence of high and rising real interest rates (the blue line) and flat to inverted yield curves (the red line). Today, real rates are still negative and the yield curve is still positively-sloped. Monetary policy thus appears to pose no threat to economic growth, at least as far as the bond market is concerned. Otherwise the curve would be flat in the expectation that a recession would make it impossible for the Fed to ever raise rates from their current level.

This recovery continues to be the weakest in modern times. As I pointed out a few weeks ago, the main culprit is extremely

weak productivity gains. As the chart above shows, real disposable personal income would be about $1.5 trillion per year higher today if this had been a typical recovery. That's a lot of income left on the table, and it explains why the middle class is not happy with the current state of affairs. Trillions of dollars of prosperity are riding on the results of the November elections, with only Republicans proposing policies that could change things for the better (e.g., reduced marginal tax rates, tax code simplification, reduced regulatory burdens).

Corporate credit spreads are elevated, and that is a legitimate source of concern (see charts above). But most of the problems with default risk are found in the oil patch. Ex-energy, high-yield bond spreads today are still less than what we saw during the PIIGS crisis of 2011, and far less than the spreads we saw in the 2008 financial crisis. So it looks like the problems in the oil patch are relatively contained. And with oil prices having stabilized, spreads on HY energy debt have already tightened by 375 bps from their recent highs of 1,984 bps. Once again I note that swap spreads are still very low, which suggests the problems in the oil patch have not resulted in any deterioration in the economic and financial fundamentals. Systemic risk is still very low, and liquidity is abundant. Healthy financial markets are a prerequisite for managing and resolving economic dislocations. Today, the economic and financial fundamentals are significantly better than they were in 2008. Back then, the Fed was tight, and liquidity was in very short supply. It's a very different story today.

Markets are still very worried, of course, as the chart above shows. The Vix index is unusually high, the 10-yr Treasury yield is quite low, and equities are still down almost 10% from their highs of last May. The pattern in the above chart (i.e., spikes in the Vix/10-yr ratio coinciding with plunges in the S&P 500 index) has been repeated quite often in recent years, only to be resolved with higher equity prices as fears decline and confidence returns. The recent decline in the Vix/10-yr ratio is thus encouraging, as is the lack of evidence that the problems in the oil patch are spreading. Still, there are many ongoing calls for a sharply lower market and a worsening of economic conditions. But from what I see, there is no reason to panic. A simple continuation of what we've seen in recent years should be enough to support equity prices at current or higher levels. In the end, a

voiding recession is all that matters, as I've been saying for the past three years.